Echoes Of New Century’s Collapse Amid Sudden Firesale Of Real Estate Loans As One Bank Sees 40% Downside

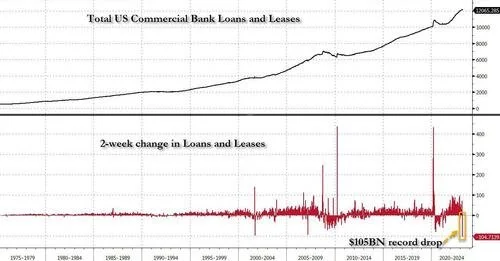

(Tyler Durden) Those who peaked below the surface of the latest H.8 statement which, as discussed previously, saw the biggest drop on record in bank loans and leases in the last two weeks of March…

… found another, perhaps even bigger surprise. As we detailed over the weekend when breaking down the weekly change in small bank loans and leases by their subcomponents, we found that whereas in the first week after the bank crisis (the one ending March 15) the bulk of the collapse in loans was in the traditionally volatile C&I space, the latest week was a surprise: that’s because while the plunge in C&I loans moderated substantially to just $6.9BN from $25BN the week before, the biggest slide was in one of the anchor pillars of the small bank sector: real estate loans.

In fact, while the biggest drop among small bank loans in the latest week was the $18.7BN decline in real estate loans, this was a continuation of the $19.2BN drop in the previous week. Combining the two weeks adds to a $37.8BN plunge in real estate loans in the second half of March. This number is notable because it is the biggest since the collapse of the country’s then-second largest subprime lender, New Century Financial in March 2007, which as most traders over 40 recall, was the catalyst that ushered in the global financial crisis, and within the year led to the collapse of Bear Stearns and, eventually, Lehman.

Of course, for the past month we have been warning that real estate and especially Commercial Real Estate is the ticking solvency time bomb within both large and small banks, now that the liquidity crisis that crushed several “small” banks has been contained courtesy of nearly half a trillion in reserve injections by the Fed. And while we previously discussed at length the coming multi-trillion CRE maturity wall, (see “New “Big Short” Hits Record Low As Focus Turns To $400 Billion CRE Debt Maturity Wall“)…

… increasingly more are also seemingly starting to notice and, what is far more ominously, are taking a page out of the Margin Call playbook and quietly selling out of their real estate loan exposure: or to quote Kevin Spacey, “this is what the beginning of a firesale looks like.”

To be sure, it’s no longer just us that are focusing on the potential of CRE to be the next market crash catalyst. As Bloomberg wrote over the weekend, “almost $1.5 trillion of US commercial real estate debt comes due for repayment before the end of 2025. The big question facing those borrowers is who’s going to lend to them?”

Well, there is another even bigger question as the video clip above suggests, but we’ll get back to it in a second.

Bloomberg quotes a recent must-read note by Morgan Stanley titled “Scaling Maturity Walls” (available to pro subs in the usual place) in which the bank’s credit strategists write that “refinancing risks are front and center” for owners of properties from office buildings to stores and warehouses, adding that “the maturity wall here is front-loaded. So are the associated risks.”

Looking at the charts below, Morgan Stanley’s James Egan writes that “roughly $400-450bn worth of CRE loans are scheduled to mature in 2023. This is on par with 2022, and both of those years are the largest on record ( Exhibit 12 ). From there it doesn’t get any easier, as maturities climb each year until 2027, reaching over $550bn.” And “while the maturity walls within other asset classes might not be very front loaded, the issue within commercial real estate is happening right now.”

As these maturities come due, Egan warns that he is left many more questions than answers, “chief among them: who is going to be responsible for refinancing these loans as they mature? That story differs depending on property type. The multifamily space has grown very reliant on the GSEs over the years. From 2023 through 2027, 46% of maturities are currently guaranteed by the GSEs. As a reminder, in the GSE space, borrowers will ask lenders for a loan, and if the property meets the eligibility criteria for agency guarantee, then the lender should generally feel comfortable that the loan will be guaranteed by the agency when quoting a rate lock. The agencies will inspect the property at different times depending on the exact program, but given that the majority of agency guaranteed multifamily properties are held by borrowers with multiple properties, there is incentive to continue to work with the agencies.”